Best 529 College Fund Advisors in Fort Myers FL (529 + Coverdell + UGMA Planning)

May 20, 2026 | By Startuprise

Follow us

Follow us Follow us

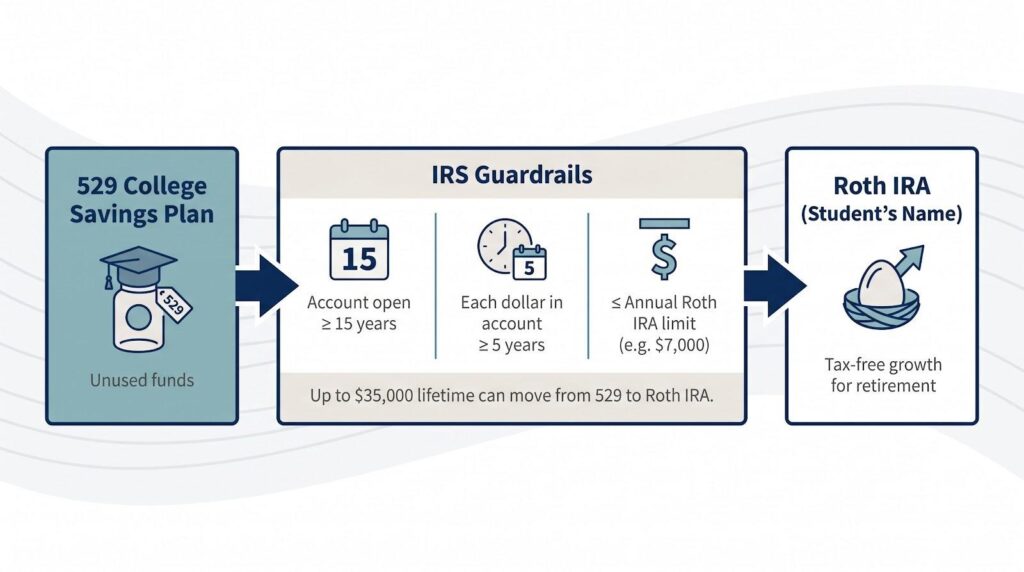

Follow usCollege costs keep rising, but a 2024 rule now lets families move up to $35,000 of unused 529 money into a Roth IRA—tax- and penalty-free. That change removes the top worry we hear from parents: “What if my kid doesn’t use the fund?”

Lee County’s head count has passed 860,000, a ten-percent jump since 2019, and newcomers want education advice tuned to Florida’s quirks—no state income tax, Bright Futures scholarships, and hurricane-season curveballs.

Below you’ll find ten Fort Myers fiduciaries, each tagged “best for” so you can quickly match their strengths to your family’s plan.

How we picked the winners

We started by mapping current search results. SmartAsset’s “Top Financial Advisors in Fort Myers” page gave us raw numbers (assets under management, account minimums, fee labels) but no clues about who actually solves college-fund puzzles.

Next, we built a scorecard around what parents and grandparents care about most today. We weighted each advisor on six fronts:

- Proven expertise in 529 and other education accounts

- Fiduciary commitment with clear pricing

- Depth of credentials and years serving Fort Myers families

- Real-world reputation, using client reviews and independent awards

- Breadth of service, including tax or financial-aid guidance

- Accessibility: reasonable minimums and a human you can meet in person or on Zoom

Each category carried a percentage weight, and we added the scores. When two firms tied, we chose the one with cleaner, jargon-free communication and locally relevant resources (think Florida Prepaid comparisons, not boiler-plate brochures). We removed any advisor who had an SEC disclosure, sold products on commission only, or never mentioned education planning.

The final top-ten list meets two non-negotiables: every pick puts your interests first and already speaks fluent “college fund” within Southwest Florida’s unique rules and rhythms.

1.Signature Financial Solutions – Best for comprehensive 529 + insurance-backed college funding

With three decades of experience advising families on education funding, Signature Financial Solutions stands out for its dual-strategy approach: combining traditional 529 plans and Coverdell ESAs with cash-value life insurance to make sure college costs are covered no matter what. Their education funding consultants build customized roadmaps for families saving across K-12, vocational, and college timelines, and clients get nondiscretionary portfolio analysis (you keep decision-making control while receiving fiduciary-grade recommendations). Licensed to sell securities in all 50 states through Osaic Wealth, Inc. (member FINRA/SIPC), they also offer exclusive access to their NextPhase™ retirement programs and a secure client portal for tracking accounts and progress. A strong pick for Fort Myers families who want a long-tenured firm guiding both the savings vehicle choice and the insurance backstop.

Pros:

- 30 years of family financial planning experience

- Both 529 plans and life-insurance-funded college strategies under one roof

- Nationwide licensing + dedicated education funding consultants

Cons:

Tampa-based, so most engagements run virtually for Fort Myers clients

The firm has served Florida households for nearly three decades, and its advice stays current. Advisors embraced the 2024 529-to-Roth rollover rule early, already weaving the tactic into plans so unused education dollars shift into a child’s retirement nest egg, a move most firms noticed only after Secure 2.0 passed. Signature Financial Solutions’ July 2025 explainer on repurposing 529 funds notes three guardrails families must clear first: the 529 must be at least 15 years old, any dollars being moved must have been in the account at least five years, and the annual rollover can’t exceed the Roth IRA contribution limit (currently $7,000). The same explainer flags that a four-year in-state degree already costs about $27,146 per year—a stark reminder that every saved dollar needs to work. For parents who want the full playbook on 529s, Coverdells, UGMAs, and Roth IRAs, Signature’s guide Building a Child's College Fund lays out each option in plain language. Macke walks clients through those same checkpoints before green-lighting a transfer.

Macke works as a fee-only fiduciary, keeping recommendations product-neutral. Expect a side-by-side look at Florida’s 529 Investment Plan versus low-fee national options; whichever offers better cost and flexibility is the one they open for you.

A typical meeting covers contribution targets, Bright Futures scenarios, and a quick stress test that confirms your retirement stays on track even after four years at Florida Gulf Coast or UF. Grandparents receive equal focus, often leaving with a gifting schedule that trims estate taxes while boosting a grandchild’s account.

No asset minimums, a clear management fee, or flat-fee planning keep access simple. Because the Fort Myers team meets clients with a concierge approach, every Lee County family can receive guidance that feels personal, not packaged.

2. Campbell Financial Partners: best fee-only advice for young families

Picture a whiteboard covered with colored sticky notes: mortgage, daycare, Roth IRA, and even a surfboard fund for weekends on Sanibel. Kathleen Campbell starts every plan that way, mapping your entire cash-flow life before she talks numbers.

That holistic first step matters. Campbell works as a fee-only fiduciary, so she can suggest any 529 nationwide. She often prefers Utah’s my529 for low fees, paired with Florida Prepaid when parents want guaranteed in-state tuition. The mix delivers both cost certainty and growth.

Because many clients are in their 30s, Kathleen skips minimums and keeps pricing clear: one flat-fee plan that covers budgets, insurance gaps, and a line item called “college runway.” She shows you how raising a 529 deposit from $150 to $200 a month can trim future student loans by five figures, and she pinpoints where that extra fifty fits without cutting date night.

Campbell also serves as translator between your tax preparer and your goals. Want the American Opportunity Tax Credit? She times 529 withdrawals so you qualify all four years. Saving for private middle school instead? She pivots to a Coverdell ESA and explains the trade-offs in two short paragraphs, not dense legal text.

Add friendly Zoom check-ins and zero product sales, and you get an advisor who feels like an accountability partner, not a gatekeeper. For young Fort Myers families juggling diapers and diplomas, that mix of rigor and relatability brings real relief.

3. Finley Wealth Advisors: best for high-net-worth, multigenerational strategies

Doug Finley likes to say wealth is a family language, and his job is to keep every dollar speaking clearly for the grandchildren and beyond.

Finley Wealth Advisors serves households with seven-figure portfolios. In this world, the college question shifts from “How do we pay?” to “How do we gift wisely, cut taxes, and stay flexible for future degrees or a fourth grandchild?”

The team often starts with a strategic front-load. A one-time $85,000 529 deposit, equal to five years of gifts at once, trims the estate, accelerates compounding, and lets parents keep control. If markets wobble, advisors lower risk inside the 529 while growth assets remain in the brokerage account, so tuition stays safe without slowing long-term returns.

Leftover funds never cause panic. Finley maps three exits: change the beneficiary, hold for graduate school, or roll up to $35,000 into the child’s Roth IRA once Secure 2.0 rules allow. Each option is stress-tested against the family’s master plan, which may include trusts, charitable scholarships, or stock-option tax timing.

Service feels white-glove yet personal. Expect quarterly strategy calls, direct access to your advisor, and seamless coordination with your CPA and estate attorney. The relationship starts around one million dollars, and fees slide below one percent as assets grow.

If your balance sheet already has commas and you want college funding woven into a broader legacy plan, Finley provides both the loom and the blueprint.

4. Massie & Associates: best tax-smart guidance for detail-oriented parents

Charles Massie holds both the CFP and CPA designations, and that blend of skills drives every recommendation.

He begins with contributions, calculating the point where 529 deposits cut future tax bills without squeezing monthly cash flow. Next, he layers in the American Opportunity Tax Credit, timing withdrawals so you claim all four years of the $2,500 benefit before tapping further 529 dollars.

When scholarships enter the picture, Massie shifts the playbook. If Bright Futures or an athletic award trims tuition, he shows how to withdraw the exact scholarship amount penalty-free, save it for graduate school, or plan a Roth IRA rollover once the Secure 2.0 fifteen-year rule permits.

Because Massie prepares many client returns, implementation errors disappear. Form 1099-Q matches school bills to the penny, and FAFSA questions on parent or grandparent 529s receive clear, compliant answers.

Fees stay transparent: a flat planning charge if you want a roadmap, or an assets-under-management option if you prefer full portfolio care. Either way, Massie focuses on tax law in plain English and a college-fund plan that captures every legal advantage.

5. The Martin Group at Raymond James: best big-firm resources with a local touch

Some families want the reach of a national brand without giving up the handshake feel of a neighborhood office. That’s exactly where The Martin Group fits.

The Fort Myers team taps Raymond James research, including college cost calculators, scholarship databases, and in-house financial-aid specialists, yet meetings still happen face to face on Summerlin Road, often with the same advisor you text during FAFSA season.

They excel when your plan needs several tools. If you already own a Florida Prepaid contract but still worry about room and board, the team layers a low-fee 529 savings plan on top, adjusts the asset mix as freshman year approaches, and shows how leftover Prepaid refunds can fund graduate school.

Grandparents receive special attention. Under the updated FAFSA, distributions from a grandparent-owned 529 no longer hurt aid eligibility. Advisors here spotted the change early and now set up “grandparent buckets” so families can draw those dollars strategically from freshman year onward, keeping need-based grants intact.

Fees remain clear: about one percent on advisory assets with no load on managed 529s. Because Raymond James also offers trust services and lending, you can move from saving to paying through a portfolio credit line or education trust without starting a new relationship elsewhere.

In short, The Martin Group pairs Fortune-500 scale with Southwest Florida hospitality. If you prefer every money question handled under one roof, they keep the umbrella open.

6. Rezny Wealth Management: best for ultra-high-net-worth families who want active oversight

Rezny’s Fort Myers office feels more like a boutique research lab than a coastal branch. Brian Rezny and his team manage portfolios starting at $2 million, and their college-fund advice matches that rigor.

For these clients, aid formulas are irrelevant; the goal is precision gifting and downside protection. Rezny often suggests seeding each grandchild’s 529 with a five-year $85,000 lump sum. The move trims estate taxes and allows the firm to adjust risk inside the account instead of relying on set-and-forget age tracks.

Active is the keyword. If markets slide six months before freshman year, Rezny shifts 529 holdings to cash and short-term bonds, locking tuition while the broader portfolio keeps compounding. Few advisors provide that hands-on rebalancing inside education accounts, and Rezny includes it in the fee.

Clients also gain multi-layer planning. A trust officer can create an education trust when 529 limits feel tight, and the investment committee maps how those trust assets interact with a charitable foundation or donor-advised fund.

Fees stay clear: about one percent of assets with a $10,000 annual minimum. That price covers white-glove reporting, quarterly strategy calls, and confidence that every education dollar receives the same disciplined oversight as the rest of your fortune.

7. Alliance Financial Group: best blend of insurance protection and college savings

Saving for college is noble; protecting that goal from life’s curveballs is even wiser. Alliance Financial Group tackles both in one plan.

The process begins with a Living Balance Sheet review. You see every inflow, outflow, and risk on one screen. From there, advisors suggest a two-bucket approach: a no-load 529 for predictable tuition and a cash-value life policy that grows tax-deferred, stays off the FAFSA radar, and adds family protection.

Many parents hesitate at pairing insurance with college funding until they see side-by-side projections. The 529 offers market growth and tax-free withdrawals, while the life policy provides guarantees and emergency access if a hurricane cuts income for a semester. Together, the buckets cover what markets and Mother Nature deliver.

Alliance’s bilingual advisors host workshops in English and Spanish, guiding parents through scholarship hacks, FAFSA timing, and the updated grandparent 529 rule. Because most compensation comes from implemented products, the upfront financial plan is often free, and every cost is disclosed before you sign.

If you want coverage and college dollars under one roof, and you appreciate face-to-face guidance from a team that teaches these ideas in local schools, Alliance turns complexity into a clear action checklist.

8. Waterstone Financial Advisory: best tech-forward planning for busy millennials

Waterstone may be the new kid on the block, but its founders left big firms with CFP badges and built a practice around how thirty-somethings actually live—mobile first, subscription pricing, zero jargon.

Your first meeting happens on Zoom with a shared screen. In twenty minutes you watch a live chart of tuition at UF, UCF, and a private option, each tied to a slider that shows what $150, $250, or $400 a month into a low-fee 529 can grow to over 18 years. Adjust a slider and the graph refreshes instantly, making trade-offs crystal clear.

Waterstone Financial Advisory tech-forward retirement and college planning website screenshot

Because Waterstone charges a flat annual planning fee, often under $3,000, there is no pressure to move your 401(k) or brokerage account. Many clients keep investments DIY but hire Waterstone for strategy and accountability. Monthly check-ins nudge you when contributions slip and cheer you on when raises lift the savings rate.

Flexibility stays baked in. Advisors often pair a national 529 with a starter Roth IRA for the child, teaching parents how the new 529-to-Roth rollover rules can future-proof unused funds. They also map how extra mortgage payments or lingering student loans affect the college timeline, so every dollar finds its most productive job.

If you manage life from a phone screen and want college planning that keeps pace, Waterstone turns complex projections into swipe-friendly action steps.

9. Merrill Lynch, the Phillips Group: best one-stop wealth and college funding hub

Some families want every money question—savings, loans, banking, even credit-card rewards—answered under a single logo. Merrill plus Bank of America delivers that convenience, and the Phillips Group turns the giant’s resources into a tailored college plan.

They begin with Merrill’s Goal Planning System, a live dashboard that shows 529 balances beside your mortgage, IRA, and checking account. Move a slider and you see, in real dollars, how boosting a 529 deposit or refinancing the mortgage changes your projected tuition gap.

RECOMMENDED FOR YOU

Why Contract Intelligence Is Becoming Essential for Modern Construction Teams

Startuprise

Mar 19, 2026

Merrill Lynch Goal Planning System integrated college funding dashboard

Because Merrill custody links to Bank of America banking, execution stays smooth. Need to pay a spring-term bill before a 529 distribution arrives? The team can open a portfolio credit line at preferential rates, then repay it when the 529 money lands, keeping you on time and on budget.

The Phillips advisors also lean into new rules. Grandparent 529s now sit in an “aid-friendly” bucket, and withdrawals can start freshman year without hurting eligibility. Leftover funds shift into a Roth IRA for the student up to the $35,000 lifetime cap, so nothing goes to waste.

The relationship starts around $250,000 in assets, and the advisory fee hovers near one percent. In return you gain 24-hour online visibility, a private-bank style service desk, and the comfort of having every financial lever inside one coordinated system.

10. Blue Chip Financial: best personal-touch advisor for first-time 529 savers

If walking into a marble-floored wealth office feels intimidating, Blue Chip Financial offers a friendlier doorway. It is a small, independent shop where your advisor greets you by name and remembers which child just earned a science-fair ribbon.

That intimacy guides the planning process. Meetings open with one question: “How much can you comfortably save each month without losing sleep?” The team then builds a budget-first blueprint, often starting with a single direct-sold 529 plan, so every dollar lands in the market rather than in sales charges.

Many Blue Chip clients are teachers, service members, and young professionals, so the advisors focus on simple automation. They help set up payroll splits or recurring bank drafts so the 529 fills itself. Annual reviews reset contribution levels against rising tuition and your latest raise.

Risk management stays on the radar without overshadowing the goal. When life or disability coverage is wise, the team explains options in plain language and discloses any commission before paperwork appears.

With no asset minimums and flexible hourly or AUM pricing, Blue Chip becomes the on-ramp many Fort Myers families need when college planning still sounds distant and complicated. You leave the first meeting with a starter plan, a clear savings target, and a phone number answered by a person, not an automated tree.

Conclusion

Each of the ten firms above brings a different strength to the college-fund conversation, from tax-smart tactics to tech-forward dashboards. Start by matching your family’s priorities—cost control, multigenerational gifting, hands-on investment management, or all-in-one convenience—to the advisor that excels in that arena. With the right partner, Florida’s scholarships, new 529-to-Roth rules, and hurricane-season curveballs all become opportunities rather than obstacles on the path to a debt-free diploma.

Recommended Stories for You

Startuprise Apr 9, 2026

Startuprise Mar 19, 2026

Startuprise May 2, 2026

Startuprise Apr 9, 2026

Startuprise Aug 21, 2025

Startuprise Jun 1, 2026

Trending Stories

How Crypto Can Help Grow Your Money: Key Financial Benefits Explained

The High-End Tool Economy: Why Quality Wins In 2026

The Essential First Steps Every New Business Owner Should Take

Startup Growth: 10 Practical Strategies to Acquire Your First 1,000 Customers

Helping Others, Helping Yourself: Why Choose Wellness as a Career

Design-Forward Pet Essentials for the Modern Home

Startup Facility Risks That Can Affect Workplace Readiness

Why Your Startup Needs Automated Infrastructure