How to Get a Personal Financial Advisor for My Job 401k Without Overpaying Fees

Jul 16, 2026 | By Startuprise

Follow us

Follow us Follow us

Follow usYour 401(k) is probably your biggest asset, yet many savers pick a target-date fund and hope. Doubts follow: Are these funds right? Am I saving enough? Should I roll everything elsewhere? We want expert help, but 1 percent “wealth-management” fees and commission-heavy pitches feel worse than no help at all.

The good news: you can secure fiduciary guidance without draining your balance. Savers who use qualified advice are far more confident: 83 percent feel on track for retirement versus 53 percent who go solo. Ahead, you’ll learn when outside help makes sense, why 401(k)s pose unique hurdles, and four low-cost ways to bring a pro onto your team.

Ready to trade anxiety for a plan? Read on.

Do you need a 401(k) advisor?

Start with an honest gut check.

If your 401(k) balance is small, the plan offers plenty of low-cost index or target-date funds, and you like fine-tuning investments on a quiet weekend, steer the ship yourself. The target-date fund already handles rebalancing, and you skip every advisor fee.

That picture changes when your dollars, and life complexity, grow. A six-figure balance, multiple retirement accounts, stock compensation, or an approaching retirement date adds moving parts most DIY investors miss. Asset location, tax timing, and required minimum distributions become high-stakes puzzles. One misstep can erase years of returns.

Behavior counts too. We panic when markets dive and chase winners at the peak. A seasoned planner offers a rational second opinion, keeping you aligned with long-term targets when fear or FOMO grabs the wheel.

Cost is the counterweight. Traditional advisors often charge about one percent of assets each year. On a $400,000 401(k), that equals $4,000 per year, money that could keep compounding in your account. Decide whether expertise, coaching, and peace of mind outweigh that drag; the self-assessment comes first.

Here is the quick rule we share with clients: If choosing funds, setting an allocation, and sticking to it feels routine, stay the course solo. If any step gives you pause, or you want a sounding board as your wealth grows, explore paid help. The rest of this guide shows how to do so without handing over the full one percent.

Why workplace 401(k)s create special hurdles

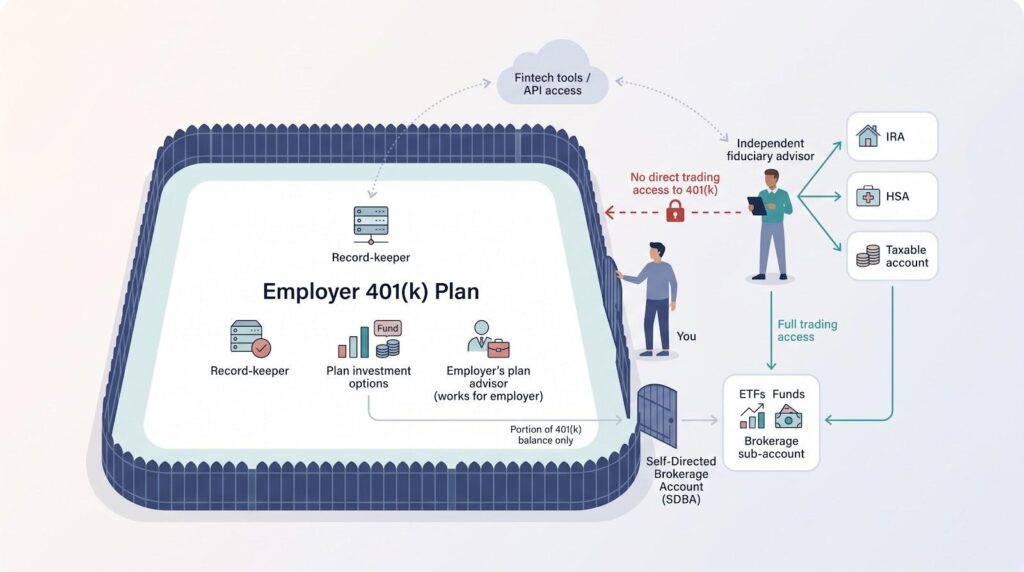

A 401(k) is not just another brokerage account. Open an IRA and your advisor can place trades and rebalance without a second thought. An employer plan is different. The record-keeper treats outsiders as, well, outsiders. Most independent planners cannot log in and trade for you; they can only hand over instructions and hope you follow them.

Industry rules often spell it out: many planners cannot directly touch a client’s 401(k), HSA, or pension, so you must ask how they will fold that held-away money into your wider plan.

The gap frustrates both sides. You handle the clicks, and the advisor worries recommendations fall through the cracks. Two work-arounds have emerged.

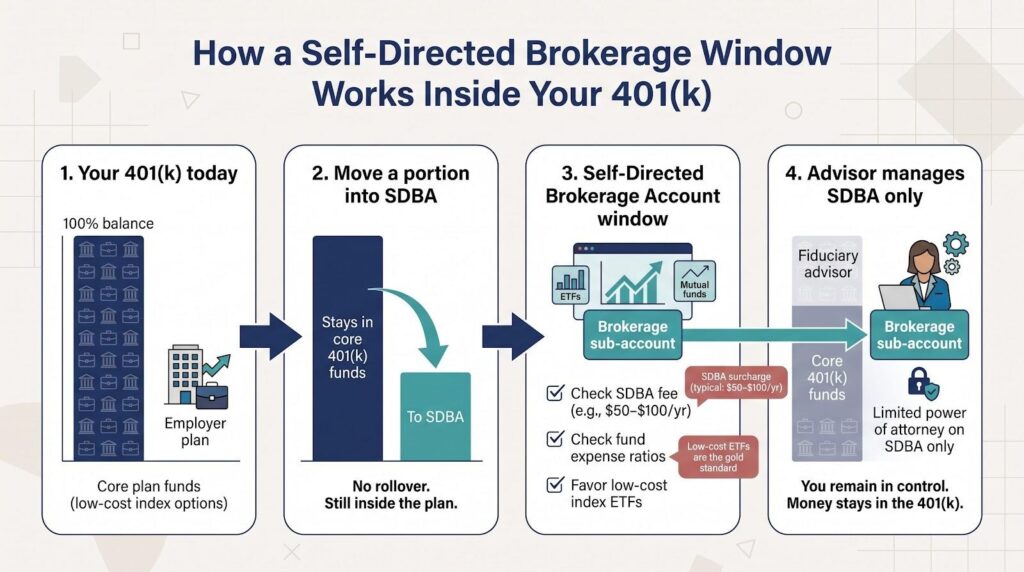

First, some companies offer a self-directed brokerage window (SDBA). Think of it as a side door inside your 401(k) that routes part of your balance to a regular brokerage platform. Once there, your advisor gains full trading powers while you keep the plan’s low-cost institutional funds for the rest.

Second, specialized fintech tools try to let planners trade inside 401(k)s without sharing your password. Major record-keepers pushed back in late 2025, citing security risks. The tug-of-war continues, so confirm that your plan allows this access before you pay for it.

Finally, recall the plan advisor who ran last week’s lunch-and-learn. They represent the employer, not you. Their guidance stays high-level and rarely tackles tax strategy or that stock-heavy ESPP you hold elsewhere. If you want someone fully on your side, you hire and pay them directly.

Bottom line: a 401(k) lives in its own walled garden. Knowing those walls exist helps you pick the right tool or advisor to reach over them.

What a good advisor will (and won’t) do for your 401(k)

Picture your 401(k) as the engine of a cross-country road trip. A skilled advisor tunes that engine, checks the tires, and plots the route, then rides shotgun to keep you from veering off course.

First, they fine-tune your asset mix. Instead of parking everything in the default fund, a planner reviews every option on the plan menu and balances stocks, bonds, and cash to match your risk comfort and timeline. They also look under the hood of your IRA, HSA, and taxable accounts so the whole portfolio works together rather than at cross-purposes.

Next comes tax choreography. A thoughtful advisor slots tax-heavy bond funds inside the 401(k), places fast-growing equities in Roth space, and times contributions or Roth conversions to trim your lifetime tax bill. Those moves rarely show up in generic plan advice.

As retirement nears, the focus shifts from growth to cash-flow math. Your advisor maps a withdrawal order that blends Social Security, the 401(k), and any rollover IRAs so you meet spending needs, satisfy required distributions, and avoid extra taxes.

Equally valuable is the emotional handbrake. When markets dive, a steady voice saying, “We planned for this,” can prevent a panic sale. When headlines hype the next hot fund, that same voice asks, “Does this help your goals?” Discipline often becomes its own return.

What they won’t do? A true fiduciary never pushes a pricey rollover, pitches high-fee mutual funds, or disappears once papers are signed. Their role is guidance, grounded in your best interest, not product sales. If an “advisor” leads with commissions, keep driving.

Strategies to get 401(k) advice without overpaying fees

1. Use a self-directed brokerage account

Think of a self-directed brokerage window (SDBA) as a side door inside your 401(k). Move, say, 20 or 30 percent of the balance into that window, and you or your fiduciary advisor can buy almost any fund or ETF on the open market.

The core 401(k) lineup stays cheap but limited. The SDBA keeps those low fees and adds flexibility, letting an outside planner trade, harvest losses, and customize your mix without forcing a costly rollover. Despite the self-directed label, one advisory firm's brokerage account management page makes the point that these windows often are not truly self-directed at all; a fiduciary can run the sub-account for you, placing the trades while you set the goals, so you gain professional oversight without uprooting assets.

Check two numbers first: the plan’s SDBA surcharge, often $50 to $100 a year, and the expense ratios of anything your advisor adds; low-cost index ETFs are the gold standard.

If the feature exists, ask HR for the paperwork, then grant your advisor limited power of attorney on that sub-account only. You remain in control, the money stays in the plan, and the advisor finally has the toolbox to earn the fee.

2. Tap your plan’s built-in help before paying a dime

Open your 401(k) dashboard and explore the advice tab. Most large providers bundle sophisticated tools many savers never notice.

Start with the robo-style allocators. You answer a few questions, and the algorithm recommends a mix and rebalances it automatically, often at no cost because the employer covers it.

Next, look for a managed-account upgrade. Many providers run full portfolio management inside the plan for roughly 0.30 to 0.50 percent instead of the traditional one percent. The fee comes straight from your account, so you see it, but it remains clear and competitive.

Do not overlook human help lines. Record-keepers now staff certified planners who will review your fund picks, contribution rate, and Roth versus pre-tax decisions over a brief call. The service is usually free, covered by plan fees. Book the call, prepare questions, and you may gain enough clarity to skip outside advice.

Remember, these resources stay plan-centric. They will not integrate a spouse’s IRA or map a college-savings plan. Still, squeezing value from what you already pay for is the smartest first move.

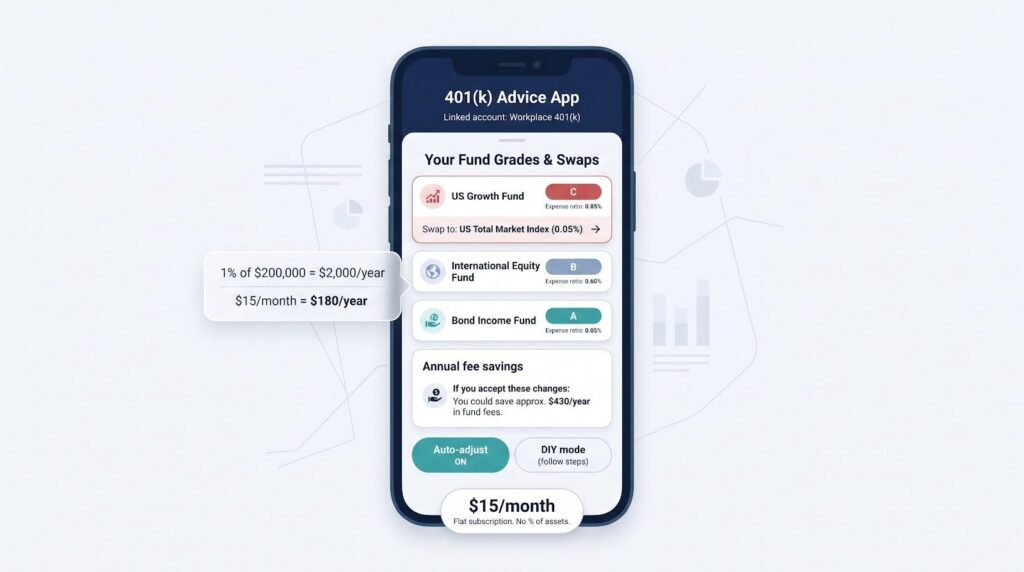

3. Try a low-cost robo or 401(k) advice app

If you love automation and dislike high percentages, a robo-advisor built for workplace plans fills the middle ground. Some third-party apps connect to your 401(k), scan the fund lineup, and swap out pricey underperformers for low-fee index funds, all for a flat monthly subscription.

RECOMMENDED FOR YOU

Other platforms rely on algorithms without taking control. They grade each fund option and provide step-by-step instructions you follow, perfect for a hands-on saver who still wants expert screening.

AI-powered planning tools also cut prices. For a one-time fee, usually between five hundred and two thousand dollars, you can upload account data, answer a detailed questionnaire, and receive a comprehensive retirement roadmap. No recurring charges, no asset minimums, no sales pitch.

Before subscribing, ask whether the platform links directly to your 401(k) provider or requires manual ticker entry. Direct links save time, but manual updates work if you refresh a few times a year.

For many investors, pairing a robo’s ongoing rebalancing with a yearly human check-in strikes the cost-value sweet spot.

4. Hire an advice-only or hourly planner when you need personal guidance

Sometimes you want a real pro, but only for a tight list of questions: Is the asset mix right? Should you raise contributions now or after the mortgage is gone? Roth conversion, yes or no? That is where advice-only planners shine.

These certified pros sell knowledge, not products. You pay a quoted hourly rate, often between one hundred fifty and three hundred dollars, or a flat project fee. They review your 401(k) lineup, model tax scenarios, and deliver a written action plan. Implementation stays in your hands, so the meter stops when the meeting ends. On a five hundred thousand dollar account, spending one thousand on a deep dive beats paying five thousand every year.

Finding them is easy. Professional directories let you filter for “hourly” or “advice-only” and show minimums, usually none. Before booking, email your latest 401(k) statement and outline questions. Preparation trims billable time and sharpens the guidance.

The payoff? You get conflict-free advice tailored to your situation, then pivot back to DIY mode. No ongoing contract, no pressure to roll assets, no surprise invoices.

Finding a truly fiduciary, fee-conscious advisor

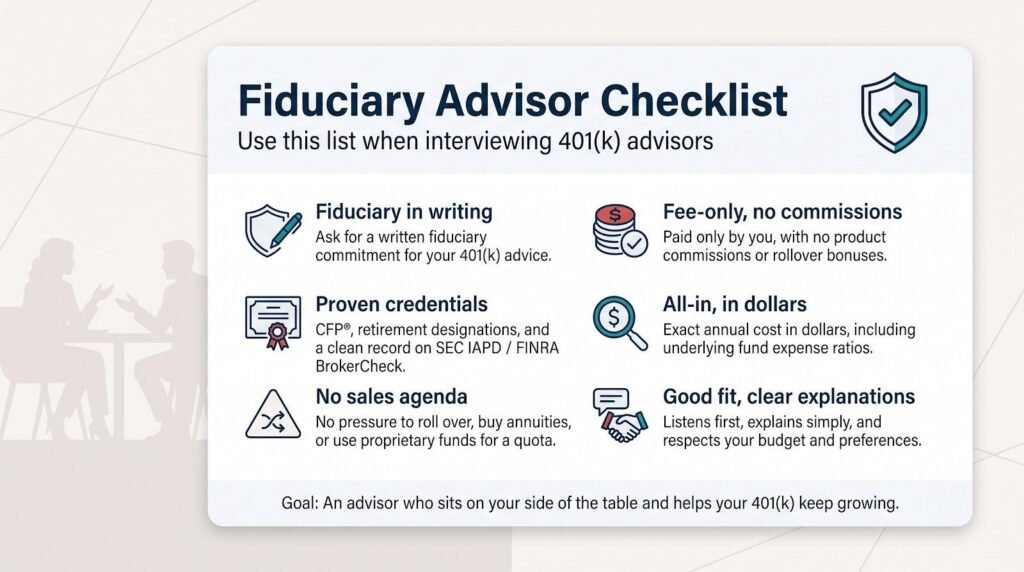

Choosing an advisor can feel like speed-dating with your life savings on the table. Start with fiduciary status. Under federal retirement law, a fiduciary must offer advice that is prudent, loyal, and conflict-free, and provide that promise in writing.

Credentials come next. Look for the CFP®, Chartered Retirement Planning Counselor, or similar marks that require ethics and continuing education. Then run the name through the SEC’s Investment Adviser Public Disclosure site and FINRA’s BrokerCheck to confirm a clean record. A few minutes of online sleuthing can prevent years of regret.

Pin down the fee. Ask, “Exactly how will I pay you, and how much each year?” Get the figure in dollars, not percentages, and insist on the all-in cost, including mutual-fund expense ratios. A clear answer builds trust; vagueness is a warning sign.

Probe for hidden incentives. Does the firm earn commissions or bonuses for rollovers, annuities, or proprietary funds? If anyone other than you funds their paycheck, conflicts can creep in. A fee-only structure removes that haze.

Finally, treat the meeting like a job interview. Share your plan’s fund lineup and ask how the advisor will fold those choices into outside accounts. Notice whether they listen first, explain clearly, and respect your budget. A good fit leaves you feeling lighter, not pressured.

The payoff: an advisor who sits on your side of the table and charges a price that lets your 401(k) keep growing.

Understanding advisor fees and trimming them to size

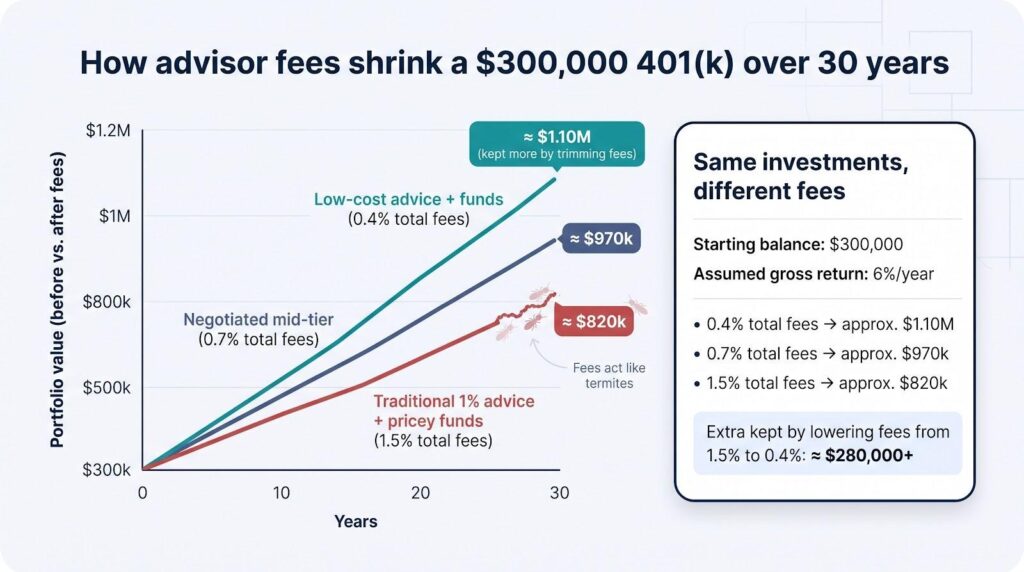

Fees act like termites. Tiny percentages chew at your portfolio year after year until real money disappears. Full-service advice often runs about one percent of assets annually. On a $300,000 401(k), that is $3,000 every year, not a one-time tune-up. Add fund expense ratios and you could lose more than four percent of every market gain before you even see it.

The math gets clearer when you convert percentages to dollars. Ask, “If my balance stays flat for the next twelve months, how many dollars will I owe you?” Then follow with, “What do the underlying funds cost?” A confident advisor answers in plain English and round numbers. Vague ranges or layered jargon are warning signs.

Next, match the service list to the invoice. Ongoing tax strategy, estate planning, and coordination across multiple accounts can justify a higher bill. A simple annual asset-allocation check cannot. If a planner quotes one percent but your needs are light, negotiate. Many firms cut the rate to 0.70 percent for larger balances or switch to a flat annual retainer. It never hurts to ask.

Watch for hidden costs. Wrap fees, trading commissions inside an IRA rollover, or high-expense mutual funds often appear as “professional picks.” Ask the advisor to favor low-cost index funds unless a specific, documented reason says otherwise. When unsure, compare each fund’s expense ratio to the nearest index alternative.

Finally, let competition work for you. Collect proposals from two or three fiduciary candidates. Share the lowest quote, without naming names, and ask others to match or beat it. Advisory fees have drifted lower over the past decade; ride that trend.

Conclusion

The goal is simple: pay enough to secure expertise and accountability, but not a penny more. Every dollar you keep stays in the market, compounding for retirement instead of lining someone else’s pocket.

Recommended Stories for You

Startuprise Dec 24, 2025

Startuprise Apr 24, 2026

Startuprise Jun 14, 2026

Startuprise Apr 28, 2026

Startuprise Apr 8, 2026

Startuprise Jun 11, 2026

Trending Stories

The Complete Guide to Cloud Phone Systems for Startups

Why Diesel is the Preferred Fuel for Commercial Fleets

Factors That Could Impact the Validity of Your Personal Injury Claim

Is It Time for Your Startup to Buy Instead of Lease

8 Ways Technology Enhances Coordination In Mobile Service Teams

The 2026 Pitch Deck: Why Your Outline Is Your Secret Weapon

6 Ways AI Receptionists Accelerate Startup Growth

The Industrialist’s Reading List: Stay Ahead of the Curve